Political-controlled infrastructure initiatives Fuel requirement for animal 1 and animal-2

Company logo

Global Civil Construction Surge: Political Control

Market for civil engineering contracts

Market for civil engineering contracts

Dublin, September 19, 2025 (Globe Newswire) – The report “Market opportunities for civil engineering contracts, growth drivers, industry trend analysis and forecast 2025 – 2034” was added Researchandmarkets.com Offer.

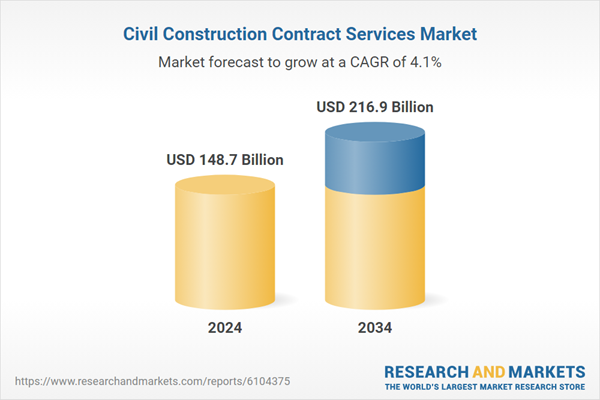

The worldwide market for Civil Construction Contract Services was rated $ 148.7 billion in 2024 and is expected to grow from 4.1% to $ 216.9 billion by 2034.

This growth is mainly driven by large -scale infrastructure initiatives of governments in North America, Asia and Europe. These national infrastructure programs aim to promote economic recovery, to support urbanization and to support them to be reliable infrastructure systems. In the Asian-Pacific region, political framework conditions such as the national infrastructure pipeline in India and the national resilience program of Japan have founded several years of demand pipelines in which EPC companies and contract service providers are essential managers.

These programs not only assign billions in funds, but also set up institutional mechanisms for a faster project permit, which further increases the demand for civil contractors. The cumulative effects of those supported by politics are a structural increase in long-term contracts, especially for animal 1 and animal 2 service providers that can scale the operations and meet compliance criteria.

Such mega-urban projects require a gradual execution, strict quality adjustment and real-time project management skills, which are usually externalized for specialized contract service companies. While the cities are modernizing, the contractors are expected not only to build, but also work under operating models, which creates a strategic shift in the value in the industry.

The construction service segment generated $ 41.3 billion in 2024 and is expected to reach USD 56.9 billion by 2034. Construction services (CMMS) dominate the market for civil engineering contracts due to its strategic role in monitoring, coordinating and optimizing every phase of the construction life cycle. Their dominance is based on the growing complexity of infrastructure projects, which increasingly contain several stakeholder environments, integrated delivery models (such as EPC and design building) as well as strict compliance with schedules, budgets and quality standards. CMS providers act as a nerve center – bridging owners, designers, subcontractors, suppliers and supervisory authorities – and ensure a seamless execution for both projects for public and private sector.

The large -scale project segment achieved $ 58.8 billion in 2024 and, due to their high capital value, their complexity and their strategic relevance for national development agents, kept a share of 39.6%. These projects such as Cross-Country Expressways, mass transit systems, industrial corridors and international airports have significantly larger budgets and longer schedules, which leads to significant contract volumes for service providers.

They require comprehensive planning, multi -phase execution and compliance with strict regulatory, security and sustainability standards. As a result, civil construction services such as project management, engineering design, cost estimate and risk reduction throughout the entire life cycle of these projects are essential, which means that the consistent demand is in several service categories.

The US market for Civil Construction Contract Services was rated $ 148.7 billion in 2024 and is to register a CAGR of 4.1% between 2025 and 2034, since it is intended to expand expansive infrastructure networks, persistent federal investments and a sophisticated ecosystem of contractors, project owners and regulatory institutions and Regulatory institutions registered. The country maintains one of the world's largest inventories for public infrastructures that extend over motorways, bridges, airports, railways and water systems that require continuous modernization, capacity expansion and improvements in resilience. This creates a consistent pipeline of projects, many of which are carried out by service-oriented models such as design builds and EPC. The scale and frequency of such developments create high -quality, multi -year contractual options and strengthen the United States as a central hub for construction service activities.

The most important actors on the market for civilian building contract services include CPB contractors, Vinci SA, Larsen & Toubro (L&T), Fluor Corporation, Bouygues Construction, Hyundai Engineering & Construction, Gamuda Berhad, ACS Group, Shanghai Construction Group Co.SkaSka from and Ferrovial.

The most important strategies used by companies on the market for civil engineering contracts to strengthen their presence include expanding their services in order to capture the entire project life cycle from design and planning to construction and maintenance.

This integrated approach enables companies to provide comprehensive solutions and improve their competitiveness. In addition, companies invest in advanced technologies such as Baim (Building Information Modeling), drones and artificial intelligence to improve project efficiency, accuracy and security. Strategic partnerships and joint ventures are also widespread and enable companies to use local specialist knowledge and access new markets.

Comprehensive market analysis and forecast

Industry trends, important growth drivers, challenges, future opportunities and regulatory landscape

Competition landscape with Porters five forces and plague analyzes

Market size, segmentation and regional forecasts

Flying company profiles, business strategies, financial insights and SWOT analysis

Key attributes:

Report attribute

Details

Number of pages

150

Forecast period

2024 – 2034

Estimated market value (USD) in 2024

148.7 billion US dollars

Predicted market value (USD) by 2034

216.9 billion US dollars

Association annual growth rate

4.1%

Regions covered

Global

Covered topics covered:

Chapter 1 Methodology and Scope 1.1 Market circumference and definition 1.2 Research design 1.3 Sources for Data Mining 1.4 Basic estimates and calculations 1.5 Primary research and validation 1.6 forecast model 1.7 Research assumptions and restrictions

Chapter 2 Summary of the Executive 2.1 Industry 360 Synopsis 2.2 Key market trends 2.2.1 Regional 2.2.2 Service 2.2.3 End of use 2.3 CXO Perspectives: Strategic Imperative 2.3.1 Main decisions for industry managers 2.3.2 Critical success factors for market participants 2.4 Future prospects and strategic recommendations

Chapter 3 Industrial knowledge 3.1 Ecosystem analysis of the industry 3.1.1 Supplier landscape 3.1.2 profit margin 3.1.3 value in every phase 3.1.4 Factor that influences the value chain 3.2 Effect forces in the industry influence forces 3.2.1 Growth driver 3.2.2 Industry pitfalls and challenges 3.2.3 Possibilities 3.3 Growth potential analysis 3.4 Future market trends 3.5 Technology and innovation landscape 3.5.1 Current technological trends 3.5.2 Emerging Technologies 3.6 Regulatory landscape 3.6.1 Standards and compliance requirements 3.6.2 Regulatory framework conditions 3.6.3 Certification standards 3.7 Analysis of Porter 3.8 Pestel analysis

Chapter 4 Competition landscape, 2024 4.1 Introduction 4.2 Market share analysis of the company 4.2.1 by region 4.2.1.1 North America 4.2.1.2 Europe 4.2.1.3 Asia -Pacific 4.3 Corporate matrix analysis 4.4 Competition analysis of the most important market participants 4.5 Competition positioning matrix 4.6 Key developments 4.6.1 Fusions and acquisitions 4.6.2 Partnerships and cooperation 4.6.3 Expansion plans

Chapter 5 market estimates and forecast according to service type, 2021 – 2034 (USD billion) 5.1 Key trends 5.2 Tree management services 5.3 Design and technical services 5.4 Project planning and development 5.5 Quality control and security management 5.6 Equipment and material supply 5.7 Site Management Services

Chapter 6 market estimates and forecast according to the contract type, 2021 – 2034, (USD billion) 6.1 key trends 6.2 Flat rate contract 6.3 Price contract 6.4 Cost plus contract 6.5 Construction contract 6.6 Time and material contract

Chapter 7 Market estimates and forecast by project type, 2021 – 2034, (USD billion) 7.1 Key trends 7.2 residential building 7.3 Commercial building 7.4 Industrial plants 7.5 Infrastructure projects 7.5.1 streets and highways 7.5.2 Bridges and tunnels 7.5.3 railways 7.5.4 airports 7.5.5 ports and marine structures 7.6 Others (energy and supply projects, etc.)

Chapter 8 Market estimates and forecast by project size, 2021 – 2034, (USD billion) 8.1 Key trends 8.2 Small projects 8.3 Medium -sized projects 8.4 Large projects 8.5 Mega projects

Chapter 9 Market estimates & forecast, after final consumption, 2021 – 2034, (USD billion) 9.1 key trends 9.2 Government and Public Sector 9.3 Private developers 9.4 Industrial organizations 9.5 real estate companies 9.6 Infrastructure development authorities

Chapter 10 market estimates & forecast by region, 2021 – 2034, (USD billion) 10.1 key trends 10.2 North America 10.2.1 US 10.2.2 Canada 10.3 Europe 10.3.1 Germany 10.3.2 UK 10.3.3 France 10.3.4 Italy 10.3.5 Spain 10.3.6 Netherlands 10.4 Asia -Pacific 10.4.1 China 10.4.2 India 10.4.3 Japan 10.4.4 South Korea 10.4.5 Australia 10.5 Latin America 10.5.1 Brazil 10.5.2 Mexico 10.5.3 Argentina 10.6 10.6.1 VAE 10.6.2 Saudi Arabia 10.6.3 South Africa

Chapter 11 Company profiles (business overview, financial data, product landscape, strategic views, SWOT analysis) 11.1 ACS group 11.2 Bechtel Corporation 11.3 Bouygues tree 11.4 China Communications Construction Company (CCCC) 11.5 CPB contractors 11.6 Ferrovial 11.7 Fluor Corporation 11.8 Gamuda Berhad 11.9 Hyundai Engineering & Construction 11.10 Laing O'Rourke 11.11 Larsen & Toubro (L&T) 11.12 Shacoria Pallonji Group 11.13 Shanghai Construction Group Co. Ltd. 11.14 Skanska from 11.15 Vinci Sa

Further information on this report can be found at https://www.rees areaterandmarkets.com/r/3p7VHV

Via Research undmarkets.com Researchandmarkets.com is the world's leading source for international market research reports and market data. We offer you the latest data on international and regional markets, important industries, the best companies, new products and the latest trends.

Attachment

Contact: Researchand undmarkets.com Laura Wood, Senior Press Manager Press@Researchandand and MarketS.com For the time hours for EST hours 1-917-300-0470 for us/ can call 1-800-526-8630 for GMT Office Hours +353-1-416-8900